Finestel’s September 2025 Crypto Market Report emphasized a month of subtle shifts as liquidity returned and institutions readied themselves for the anticipated changes in Q4.

Summary

- Finestel’s September 2025 report reveals a transition among investors towards prioritizing liquidity and structured investments as the market stabilizes within a policy-driven landscape.

- While Bitcoin and Ethereum remained dominant, there was a gradual movement of capital toward DeFi, tokenized assets, and yield-oriented strategies with solid fundamentals.

- Improved regulatory clarity across major jurisdictions enhanced confidence, promoting cautious investments in compliant projects and fostering collaboration between banks and blockchain initiatives.

- September was defined by a preparatory phase where discipline overshadowed momentum, with investors focusing on building positions rather than pursuing market rallies.

Revived Risk Appetite Across Assets

Finestel’s September 2025 Crypto Market Report indicated that while the month appeared tranquil, it significantly shifted investor sentiment.

The turning point came with the U.S. Federal Reserve’s decision on September 18 to lower interest rates by 25 basis points, marking the first reduction since March 2024 amid several weakening indicators. Job creation fell to 258,000, and consumer confidence reached its lowest level since 2023.

Chair Jerome Powell refrained from providing explicit future guidance, yet the Fed’s projections indicated internal divisions, with some members anticipating further rate cuts by year-end.

Equity markets interpreted this decision as a cue to gravitate back toward growth assets, leading the Nasdaq to climb 3.4% in the subsequent week, reflecting a renewed adventurous mindset among investors.

Crypto traders, known for their swift response to changes in liquidity and policy, noted a $3.1 billion rise in stablecoin inflows for the month, signaling new liquidity entering the ecosystem, even if it wasn’t immediately utilized.

Let’s explore the report further to understand the market’s trajectory amid these shifting dynamics.

Bitcoin Steady, Ethereum Rising

According to Finestel’s report, Bitcoin (BTC) and Ethereum (ETH) provided market stability throughout September, while capital began to redistribute beneath them.

Bitcoin fluctuated within a narrow range of $110,000 to $117,000, with the BTC Volatility Index settling at 3.05%, the lowest in five months, reflecting an unusual level of stability in a market influenced by emotions.

Over 300,000 BTC were exchanged within this range, with new accumulation zones forming around $111,000 to $113,000, while larger holders sold near the upper threshold.

In contrast, Bitcoin’s share of the total market cap dipped from 59.1% to 58%, indicating that traders were exploring options beyond their core holdings without fully relinquishing them.

Ethereum emerged as a focal point in the pursuit of yield and structured assets. By the end of September, it reached $4,480, reflecting a 3.8% increase for the month, bolstered by a staking participation rate of 30.1% of total supply. Significant contributions came from Lido (LIDO) and EigenLayer (EIGEN).

Beyond staking, Ethereum’s role as a foundational financial infrastructure strengthened. Maple Finance (SYRUP), MatrixDock (XAUM), and OpenTrade expanded their issuance of tokenized bonds and credit assets directly on-chain, bridging decentralized networks with traditional finance.

The influx of capital into non-mainstream cryptocurrencies accelerated throughout the month. Pendle’s (PENDLE) total value locked surged to nearly $7 billion as institutional users sought structured yield on-chain.

Solana (SOL) and Avalanche (AVAX) benefited from renewed ETF-related interest and integrations connecting blockchain data to artificial intelligence applications. Near Protocol (NEAR) followed suit with partnerships centered on machine-learning data verification.

BNB Coin (BNB) rose 12% as Binance approached a resolution regarding U.S. legal matters, while Chainlink (LINK) continued its steady growth through new staking opportunities and broader application in reserve verification systems.

The derivatives market dominated trading activity, accounting for more than 70% of total volume. BTC options open interest soared to $18.2 billion as traders positioned themselves ahead of the September 26 expiry known as “Three Witches Day,” when futures and options typically settle simultaneously.

DeFi and perpetual DEX tokens emerged as the month’s most dynamic segments, with Aster (ASTER) skyrocketing by 1,851% and Avantis (AVNT) increasing by 152%, reflecting heightened interest in decentralized derivatives and event-driven trading strategies.

Discreet Repositioning Among Major Investment Firms

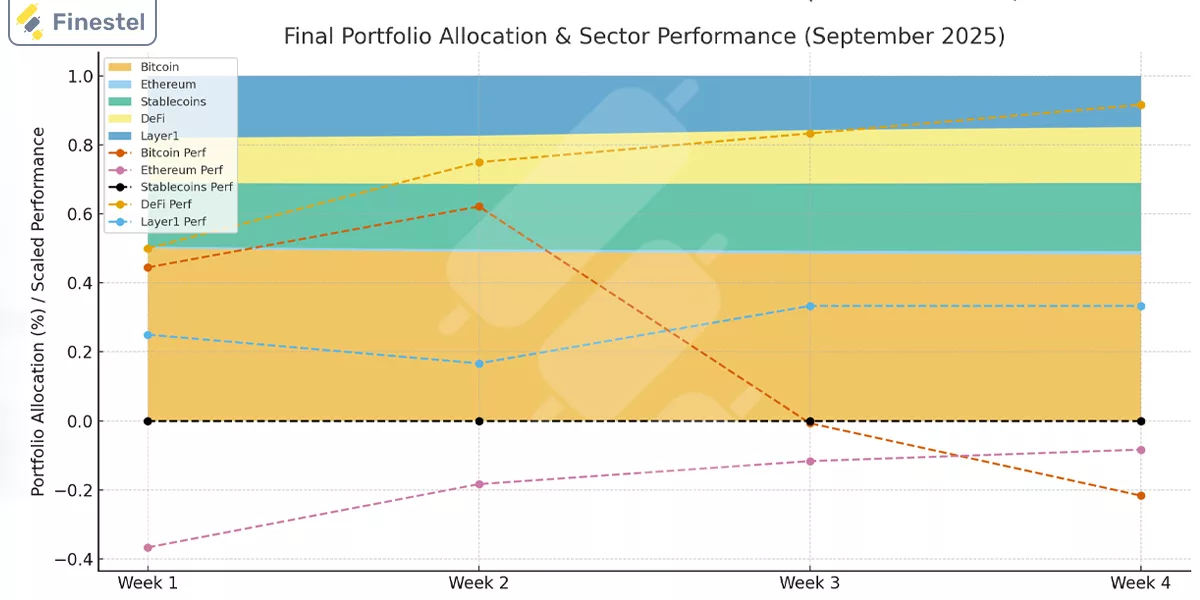

Bitcoin and Ethereum continued to form the backbone of institutional portfolios, although their combined market share decreased from 50.5% to 48.2%, while stablecoin allocations expanded to 19.8%, providing managers with liquid reserves for flexibility during changing market conditions.

Allocations toward DeFi and real-world asset protocols rose to 16.2%, while investments in alt layer-1 and narrative-driven projects remained stable at approximately 15.8%.

ETF flows indicated a resurgence of optimism, with Bitcoin and Ethereum exchange-traded funds registering $1.37 billion in net inflows during September, primarily from BlackRock and Franklin Templeton.

Infrastructure advancements also progressed. Fireblocks established partnerships with HSBC and Société Générale, strengthening the connection between banking systems and digital asset storage networks.

Corporate treasuries contributed to a gradual upward trend, with several firms incrementally increasing their Bitcoin holdings, viewing them as reserves akin to gold rather than purely speculative investments.

Policy advancements reinforced that confidence. The U.S. moved toward resolving the Binance case, alleviating a sentiment-weighting concern. The U.K. passed its Digital Securities Regulation Bill, clarifying the operation of on-chain instruments within existing securities frameworks.

The EU made progress with MiCA implementation, while South Korea aligned its stablecoin frameworks with those of the EU. Laos unveiled a 300-megawatt Bitcoin mining initiative aimed at attracting global investment.

Trading behavior during September exhibited a consistent and measured approach. Professional desks limited losses per sleeve to 6–8% while maintaining portfolio risk below 10%.

Finestel framed the outcome as one of stability. Institutions re-entered the market under established rules, structured approaches, and capital discipline—qualities that had previously been lacking.

The market setup as October approaches resembles one poised for confirmation rather than pursuing speculative trends, testing whether this stability can translate preparation into tangible progress.